I watched a video of a guy on Youtube giving his reasoning for taking Social Security at 62 as opposed to later. You can find that video here. I actually agree with his assessment except for one major thing…he doesn’t say if he’s married or not. If you’re married, the equation changes dramatically.

So I asked my friendly local AI program, ChatGPT to model a couple strategies for me which I share below. Now, first off, if you’re relying on AI to do all your dirty work, you’re wrong! AI gets a lot of stuff incorrect. I’ve had errors across the board in Grok, ChatGPT and Claude, the three AI programs I use regularly. So a word to the wise, you better have some knowledge of what you’re asking the program to solve for so it doesn’t give you false information.

In fact, in the “discussion” I was having with Chat, that’s what I call it, we’re on first name basis btw, it was so blatantly wrong, I had to ask it to rerun the numbers over and again. After a couple times of the numbers consistently showing what I was expecting to see, I was satisfied with its results. Even better though is that because the simple errors it continues to make I know it’s going to be many years before we’re all doing manual labor in the fields at the behest of our AI overlords.

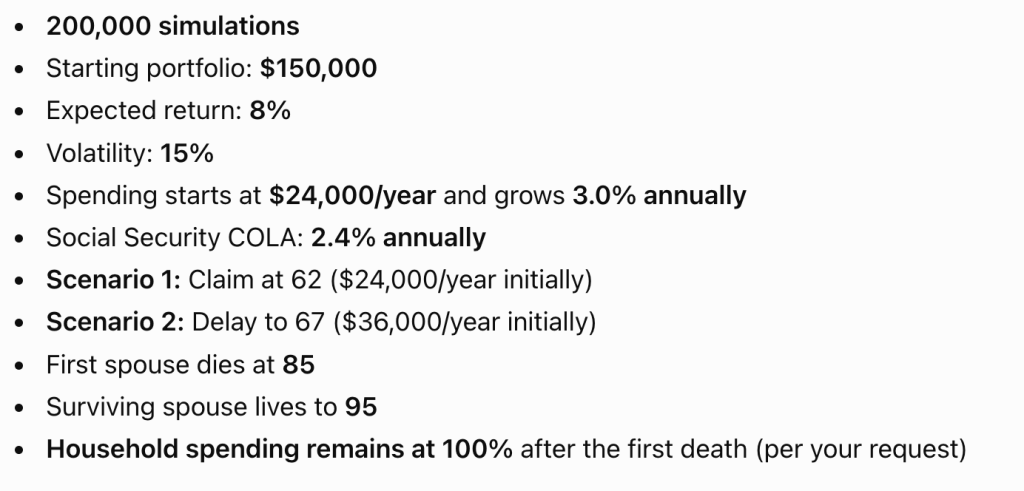

So what I wanted to compare was two scenarios with these inputs:

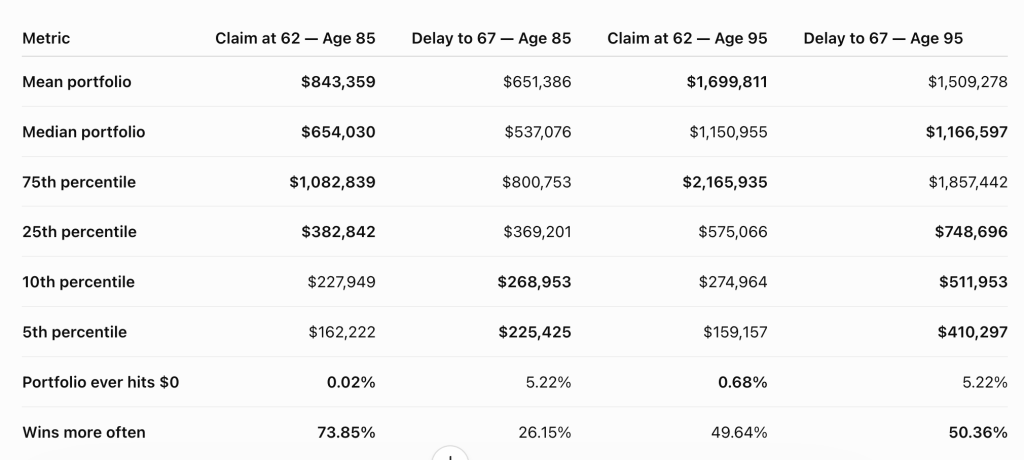

If you’re married it’s not just good enough to see what Social Security strategy works best for the first life, but we need to cover the second life too, up to the age of 95. Here is what we come up with:

At age 85, claiming at 62 wins most of the time and has higher mean/median. But delaying has better 10th and 5th percentile outcomes.

By age 95, the survivor benefit makes it almost a coin flip on win-rate, while delaying clearly improves the lower-end outcomes.

The results are clear; Take it early if one is only going to live until 85, nearly 3/4 of the time you did better. But if you, or your spouse in this case, survive another ten years, the delaying provides significantly more downside protection which you can see in lower percentile balances.

I’m not convinced we’ll get a portfolio return that averages 8%. In fact, when I’m crunching numbers for clients I use between 5% to 6% expected rates of return. So I asked ChatGPT to calculate the results with a 6% assumed rate of return and still a 15% standard deviation. But for fun I also asked for the results if we used a 10% rate of return too.

| Expected Return | Age | Metric | Claim at 62 | Delay to 67 |

|---|---|---|---|---|

| 6% | 85 | Mean | $514,520 | $453,511 |

| 85 | Median | $421,585 | $384,669 | |

| 85 | 25th percentile | $251,596 | $264,716 | |

| 85 | 10th percentile | $149,045 | $184,046 | |

| 85 | Claim 62 wins | 53.2% | 46.8% | |

| 95 | Mean | $813,536 | $906,931 | |

| 95 | Median | $561,202 | $713,496 | |

| 95 | 25th percentile | $256,979 | $430,126 | |

| 95 | 10th percentile | $92,545 | $244,351 | |

| 95 | Claim 62 wins | 25.6% | 74.4% | |

| 8% | 85 | Mean | $841,522 | $650,443 |

| 85 | Median | $652,927 | $536,235 | |

| 85 | 25th percentile | $381,759 | $369,204 | |

| 85 | 10th percentile | $227,351 | $268,415 | |

| 85 | Claim 62 wins | 73.8% | 26.2% | |

| 95 | Mean | $1,698,559 | $1,509,140 | |

| 95 | Median | $1,150,618 | $1,164,411 | |

| 95 | 25th percentile | $574,480 | $746,533 | |

| 95 | 10th percentile | $274,370 | $510,905 | |

| 95 | Claim 62 wins | 49.4% | 50.6% | |

| 10% | 85 | Mean | $1,346,669 | $951,568 |

| 85 | Median | $1,006,839 | $759,692 | |

| 85 | 25th percentile | $585,944 | $519,990 | |

| 85 | 10th percentile | $351,356 | $380,262 | |

| 85 | Claim 62 wins | 88.2% | 11.8% | |

| 95 | Mean | $3,365,157 | $2,584,589 | |

| 95 | Median | $2,222,696 | $1,924,082 | |

| 95 | 25th percentile | $1,123,988 | $1,234,991 | |

| 95 | 10th percentile | $555,458 | $853,165 | |

| 95 | Claim 62 wins | 73.2% | 26.8% |

As you can see the lower the expected rate of return and the longer life expectancy, the greater the benefit in delaying. It really comes down to that.

So, while that guy in the cited video makes complete sense as to his reasoning of taking Social Security early, remember, your reasoning is much different if you’re married or if you will live beyond your life expectancy. Just keep that in mind when planning for Social Security.

Blessings,

Josh 6/29/2026