by Josh Scandlen | May 23, 2026 | Uncategorized

Here are the number of Americans with over $1 million in INVESTABLE assets, excluding home values. Here are the number of Americans over 30 who have over $1 million in investable assets. Here are the number of Americans over 65 with over $1 million in INVESTABLE... by Josh Scandlen | May 18, 2026 | Uncategorized

Seven Short Conversations That Explore Both Sides With Evidence Cited and Common Errors Corrected By Albert Clarke, A.M. Secretary for seventeen years of the Home Market Club Chairman of the U.S. Industrial Commission, 1898–1902 Modernized Edition • 2026 A clear,... by Josh Scandlen | Mar 30, 2026 | Uncategorized

One of my main objectives being online is to get my fellow right wingers to live in reality, not made up globalist fear mongering Unfortunately, most on the right still believe what Milton Friedman said about inflation. “Inflation is always and everywhere a...

by Josh Scandlen | Mar 25, 2026 | Uncategorized

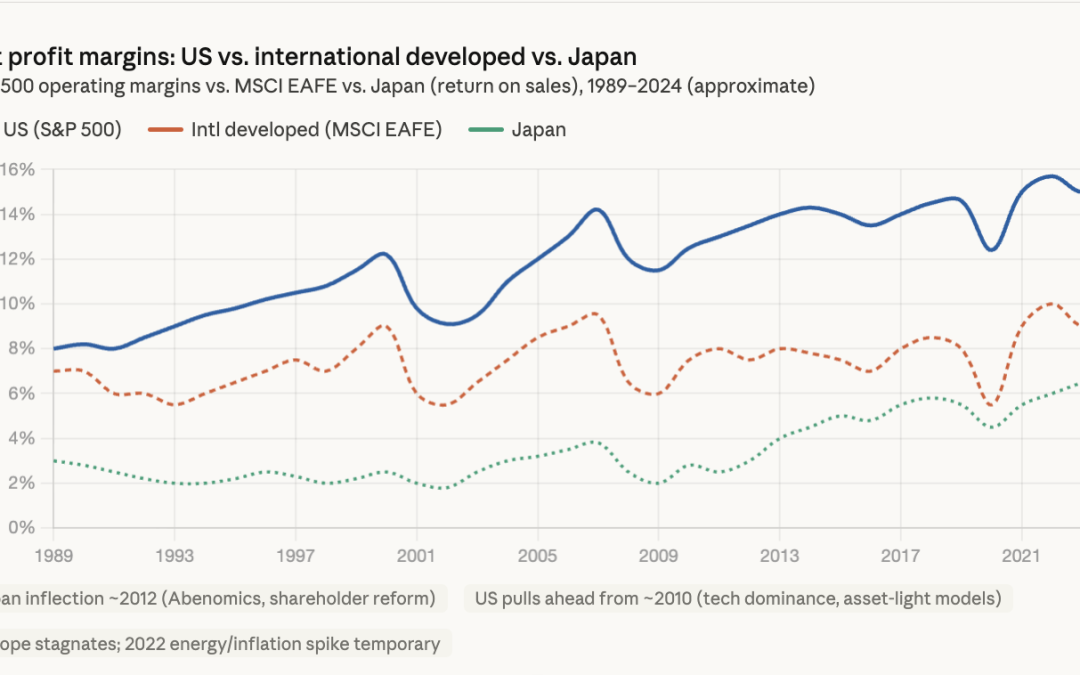

A few big themes jump out across the 50-year span. The US structural breakout after the GFC. From the end of WWII through roughly 2000, US corporate profits as a share of GDP largely ranged between 5% and 7%, but since the 2008–09 financial crisis they climbed to... by Josh Scandlen | Dec 9, 2025 | Uncategorized

Ben Johnson, CFP®, RLP®,AEP®,MS Providing Clarity, Confidence, and Peace of Mind to your Financial Plan, so you can Enjoy Life Now and In the Future. December 9, 2025 Picture “financial planning,” and most likely you imagine spreadsheets, budgets, and the vision...