By: Chris Barfield

(Another great article from Chris Barfield over at BarfieldFinancial.com. I HIGHLY suggest you subscribe to his newsletter.)

Everyone is looking for something they can do to make a big impact in their personal finances. This article is one of those things. I’ll warn you though–this is long. And it’s also boring. There’s no getting around it. But it is also something you can do immediately that could save you thousands of dollars that could then be invested elsewhere. Please set aside 10 minutes to read it!

If it gets too long and confusing, fine. Just send the article over to a life insurance agent and ask if he can do better than FEGLI. If he can’t, he’d be the first one I’ve ever heard of. FEGLI is often considered to be the most expensive insurance on the planet.

(And if you’re a life insurance agent or CFP reading this, please take some time to understand FEGLI, so you can help federal employees with better policies. It would be worth creating that niche in your industry.)

I would argue that without a doubt, FEGLI is the most confusing benefit we federal employees receive. If you are like most, you aren’t even really sure how much you’re paying for it. Or what exactly your survivor will get were you to pass away. Let me show you what I (and many others) have done. At the risk of sounding like an annoying commercial:

I saved myself almost $30k over a 20-year period by switching to a private insurance policy. And I got more coverage. True story. Read below.

I hear a LOT of myths being spouted about FEGLI.

The following are the facts:

Different Components of FEGLI

FEGLI is a multi-layered life insurance policy. It’s not as simple as “You pay $500 a year, and you get $500,000 of coverage”. It’s got a lot of parts to it—some automatic, some optional. Some parts the government subsidizes the cost, others you pay the whole premium. It’s also not a policy with a fixed cost. The rates change based on how much you make, as well as how old you are. So, it can get confusing pretty quickly. Which might explain why some employees keep it long after it has become one of the most expensive policies you can find anywhere. I will make it un-confusing if you’ll give me a few minutes…

Here are the 4 different parts, or coverages, of FEGLI (Basic, Options A, B, and C):

BASIC

Basic coverage is the cheapest part of FEGLI. The government pays 1/3 of the premium cost, while we pay 2/3.

(By the way, “premium” simply means your “cost” or “payment” to have the insurance. Don’t let financial jargon get you hung up. These premiums come out of our check every bi-weekly pay period. Note however, that most private insurance companies quote premiums in either monthly or annual costs. So make sure you compare apples to apples. Don’t compare bi-weekly premiums to monthly premiums.)

Currently, what federal employees pay is $.15 per $1,000 of coverage per pay period. If calculated monthly, this premium is $.325 per $1,000 of coverage.

Ok, so how much coverage do I have?

If you are under 35 years of age, your coverage is equal to 2x your salary + an extra $2,000. If you are 35-45 years old, the coverage decreases 10% every year until it is 1x your salary + an extra $2,000. Once you are over 45, it is simply the 1x your salary + $2,000. So, you can see from just this small example, your rates go up as your coverage goes down the closer you get to 45. Then it stabilizes.

EXAMPLE: Conner is 33 years old and has a salary of $45,500. How much Basic coverage does he have and how much does it cost him? FEGLI rounds up salaries to the next whole $1,000, so Conner would have $46,000 x 2 (because he is under 35), for a total of $92,000, plus the extra $2,000 for a grand total of $94,000. Since the Basic rate is $.325 monthly (or $.15 per pay period) per $1,000, Conner’s premiums would be $15.60 per month, or $7.20 per pay period. The 2X pay extra benefit for being under 35 is automatic; there is no chargefor this. So Conner’s premiums are based solely on $48,000 ($45,500 rounded up + extra $2,000).

The important point to note about Basic coverage as opposed to the other coverages we will discuss in a minute, is that Basic rate is fixed. It does not increase based on age. It does increase as your salary increases, because your coverage is tied to your salary, but the basic rate of $.15 per pay period/$.325 per month is fixed.

Basic is relatively cheap (by FEGLI standards), because it is government subsidized.

The following are Optional Coverages and increase based on your age. (Option B increases on both your age AND your salary.)

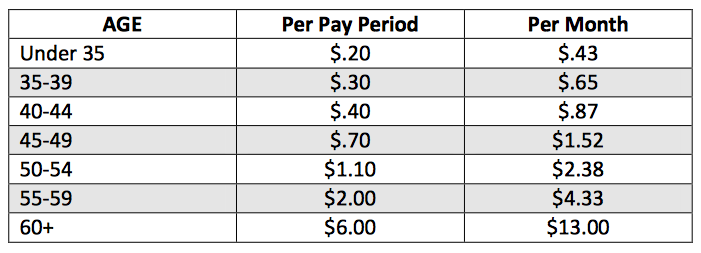

Option A

Option A is simple. It provides $10,000 in additional coverage for the employee, and like its name implies, is optional. These rates, unlike Basic, increase as you get older. They are currently:

EXAMPLE: Mike is hired by the Secret Service at 22 and wants to sign up for FEGLI Option A. He will have to pay only $.20 a pay period, or $.43 a month for this extra coverage. If Mike were 55 and still had this coverage, he would be paying $2.00 a pay period or $4.33 a month. Unlike Option B, Option A is not per multiple of $1,000. The rate is for $10,000 of coverage.

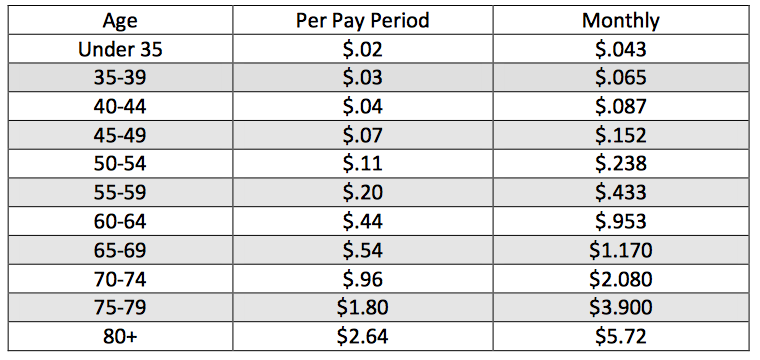

Option B

This is the coverage most commonly discussed in federal law enforcement. This is the 1x to 5x your salary you often hear people discussing. Like Option A, it is relatively inexpensive during the younger years, but becomes progressively more expensive as you get older. Unlike the Basic coverage we discussed, we pay 100% of Option B coverage; the government does not subsidize any of it.

How expensive is it? Here are the current Option B rates, which are based on age:

NOTE: Remember this rate is per thousand. So, if you have 5 times your salary, find how many thousand that will be and multiply it to find the rate.

EXAMPLE: Jennifer is 48 years old and has 5 times her salary; her salary is $134,359. She is paying $102.60 a month (135 x 5 x $.152), or $1,231.20 a year. In two years when she turns 50, those premiums will jump to $160.65 a month (135 x 5 x $.238), or $1,927.80 a year. If Jennifer still has FEGLI at 55, the new cost will now be $292.28 a month (135 x 5 x $.433), or $3,507.30 a year. I will say this more than once, but this is the minimum her premiums will be. Most employees will have their salaries go up over a 7-year period with raises and WGIs, making their premiums even higher.

NOTE: For Option B, FEGLI only rounds up to the next $1,000; they do not then add an additional $2,000 like in Basic Coverage.

Hypothetical Comparison of Private Insurance vs FEGLI

Here is a hypothetical example (but one using real numbers I acquired from USAA) for a 37-year old male in excellent shape (Keep in mind that in the private sector, women’s premiums are often cheaper than men’s.)

PRIVATE POLICY:

$1,000,000 policy, 20-year level term. Premiums: $559.80 a year. Multiply that by 20 years for a total cost of $11,196.00. So under $12,000 for $1,000,000 of coverage from age 37 until mandatory retirement at 57. (Just to explain some of the nomenclature: level term insurance means that the premiums are fixed, or level, for the term. They do not go up. It also indicates there is a set term, or time frame, where the policy is in effect—in this example 20 years. After 20 years, if you are still alive, the policy expires and you have no coverage. You do not get any of those premiums back. It is much like traditional car insurance. And it is very different from whole life insurance, which we will not discuss here.)

FEGLI POLICY:

Hypothetical 37-year old male. Salary: $118,807.50 with LEAP. Basic coverage: $121,000 (remember: they round up to the next $1,000 and add $2,000).

Monthly Basic premium: $39.33 (121 x $.3250). This equates to an annual premium of $471.90. Multiply this by 20 years for a total Basic Premium expense of $9,438.

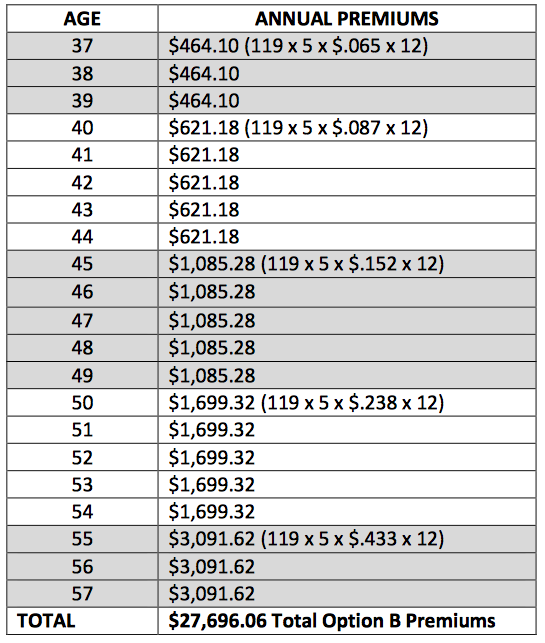

Let’s assume our hypothetical male elected Option B at 5x his salary. How much would those premiums be? Because they are based on age, we will have to break down the different rates at each age. Also, remember that for Option B, FEGLI uses salary rounded up to the next $1,000, but doesn’t include the extra $2,000. So, here goes:

Total cost of 20 years of FEGLI Policy:

20 years of Basic premiums: $ 9,438.00

20 years of Option B premiums: $27,696.06

Total FEGLI premiums for 20 years: $37,134.06

Total USAA premiums for 20 years: $11,196.00

Savings over the 20-year period: $25,938.06

Let’s note a few things about this example:

Again, understand that the FEGLI premiums are the MINIMUM you will pay. As your salary will certainly continue to go up over the next 20 years. Remember that as your salary goes up, so do your premiums as they are tied to your coverage, which is based on your salary.

$1,000,000 in coverage is more than this 37 year old would currently have, since his total coverage would be a little less than $800,000 ($119,000 x 5, plus the basic, plus part of the increased basic coverage for being younger than 45). Bottom line: more coverage, way less cost.

So, maybe you’re saying, “That’s a hypothetical example—maybe the real world won’t work exactly like that.” Fair enough. Let me give you my own, personal example with my real numbers.

Six years ago, I switched from FEGLI to private insurance after comparing the costs between the two. I was 41 at the time. I switched to a 20-year level term policy. Over a period of time between 41 and 61, my FEGLI total premiums would have been $59,818.20. (Actually they would be substantially more than that because my salary is already a lot higher now than when I was 41.) Total private insurance premiums will only cost $33,600 over that same time. This is for more coverage than FEGLI.

Because of that switch, I will save a little over $26,000 in premiums over that 20-year period. In other words, FEGLI cost $26,000 MORE than my private insurer. I also took out a lot more insurance coverage than FEGLI was giving me; if I were to have gotten the same coverage, my savings would be even more.

OPTION C

Option C is for insuring your spouse and/or children. Option C comes in multiples of $5,000 for your spouse and multiples of $2,500 for your children. You can elect anywhere from 1 to 5 multiples for each one of them. For example, you could select 3x for your spouse and 5x for each of your children. This would equate to $15,000 of coverage for your spouse and $12,500 of coverage for each of your children. For children to be eligible for this coverage, they must be your dependent and they must be under the age of 22. If you are interested in Option C, you can view the rates here.

FEGLI Calculator

RETIREMENT

If you’ve stuck with me this far, congrats. It’s a lot to digest. Everything above has been discussing a current federal employee. So, what happens when you retire? Do you get to keep FEGLI? Do the rates go up? Let’s break it down since each part is dealt with a bit differently. This will be similar to above.

Basic Coverage

As long as you have kept FEGLI for the 5 years prior to your retirement, and separate on an immediate annuity, you can keep it into retirement. Since you’re not working any more though, and the premiums are based on your salary, what salary will FEGLI use to calculate your rate? The answer is your last pay rate at retirement. Basic coverage, you will remember, at this age, means 1x your salary. So, whatever your last salary was at retirement is the coverage you will receive. However, the rates can get a little more complicated in retirement. Prior to retirement, you were paying $.3250 a month per $1,000 of coverage. At retirement, you have to start making some decisions, because coverage costs depend upon the amount of Basic coverage reductions you select.

“Ok, what’s a reduction?”

When you go to fill out all of your retirement paperwork, included in the stack will be an SF 2818 Continuation of Life Insurance Coverage form. On Section 8 of that form, you will have to choose a 75% Reduction, a 50% Reduction, or No Reduction. If you choose a reduction, your coverage will be reduced the month after you turn 65. Prior to that time, your coverage continues as it did during your employment, although at different rates (see below).

Example: Mark retires at 50 years of age and elects a 75% reduction. From age 50 to age 65, Mark continues to pay $.3250 per $1,000 for his Basic coverage. Neither the coverage nor the premium changes prior to age 65.

If Mark retires at 50 and elects a 50% reduction, from age 50 to 65, the coverage is not reduced, but the premium is now $1.0350 per $1,000 of coverage.

If Mark retires at 50 and elects no reduction, from age 50 to 65, the coverage is not reduced, but the premium is now $2.4550 per $1,000 of coverage. So, you can see how expensive the coverage can be.

So, what happens at age 65?

Based on your election you made all those years ago when you retired, both your premium and your coverage may change. Keeping with our example above, If Mark elects the 75% reduction, his Basic premiums go away at age 65. He doesn’t have to pay any more premiums for Basic coverage. It’s now free. The downside is that the coverage starts to reduce.

The coverage amount (remember 1x salary) is reduced by 2% each month until it reaches 25% of his salary. It then stays at that amount for the rest of his life. So, free Basic coverage = 25% of your salary in retirement. This is why it is called a 75% reduction—the coverage is reduced by 75%. The premiums are free.

The second option is the 50% reduction. An annuitant (retiree) pays the increased $1.0350 monthly for full Basic coverage until their 65th birthday and then coverage begins to reduce similar to the previous example. Unlike the 75% reduction though, under the 50% reduction, coverage is reduced by 1% a month (as opposed to 2%) until it bottoms out at 50% of your initial coverage. The other difference? It’s not free. But it’s cheaper than he had been paying. Now the retiree pays $.71 a month per $1,000. Both the premiums and the coverage continue until death or until they are cancelled.

The last option is no reduction.

As the name implies, Basic coverage is not reduced upon turning 65, it continues for life at the 1x salary we have been referencing this whole paper. You can probably guess that this is the most expensive option. You’re right. It’s $2.13 a month per $1,000. For someone with an ending salary of $140,000, this equates to an annual premium of $3,578.40 (140 x $2.13 x 12 months).

Here’s a chart to help summarize what happens to Basic coverage in retirement:

Option B in Retirement

Again, on SF 2818, you will have the opportunity (in block 10) to adjust your Option B insurance. It is similar to Basic except there are only two options: Full Reduction or No Reduction. Luckily it is a bit simpler to calculate.

Full Reduction

The annuitant pays the same rates as Option B listed for current employees until they turn 65. At that point the premiums cease and the insurance becomes free. The downside? The coverage eventually ceases as well. Beginning the month after your 65th, coverage decreases 2% a month until it’s zero (50 months later).

No Reduction

The annuitant pays the same rates as Option B rates listed above for the rest of their life. Coverage is never reduced, although as you can see from the table, the rates will continue to rise based on age. If you still have Option B unreduced and you make it to 80 years of age, you might wish you hadn’t. You’ll be paying $5.72 per month per $1,000 of coverage. If your last salary was $130,000, Option B at 5X your salary would be $3,718 a month, or $44,616 a year.

Other Options in Retirement

Options A and C are also affected in retirement. Because they are the least common and this thing is long enough already, I’ll leave them out. If you are interested in looking up their rates for annuitants,they are available at the following OPM link.

FEGLI- Is it all bad??

It seems like I’ve just been focusing on the negative aspects of FEGLI-the high cost. But aren’t there some good things about FEGLI? Yes. It is easy to get coverage for federal employees. It pays for everything, including acts of war. Some insurance companies exclude certain activities and certain professions are limited in the amount of coverage they can get, to include law enforcement, depending on the company.

At younger ages and younger salaries, FEGLI is not terribly expensive. And, as long as the government remains solvent, you can be guaranteed that FEGLI will pay out.

If you have had cancer or serious medical conditions, perhaps you will have a tough time finding private insurance that is affordable. In that case, FEGLI may be your best option. But please talk to someone about it.

If you are terminally ill (expected to live 9 months or less), you can cash in your FEGLI Basic coverage to have money paid directly to you (not to a survivor). This is done by completing form FE-8 Claim for Living Benefits, available from the Office of Federal Employee’s Group Life Insurance.

There are probably other benefits to FEGLI as well, but the big negative is the cost. And that cost is one that employees often don’t realize since it sort of gets lost in the raises and Within Grade Increases over the years. Seriously–have you ever dissected your leave and earnings statement to see what you’re paying for FEGLI and what you are getting for that payment???

Summary

FEGLI consists of 4 parts: Basic, Option A, Option B, and Option C. Basic is subsidized by the government—they pay 2/3, we pay 1/3. This makes Basic the cheapest part. Option B is the most common in law enforcement and gets very expensive as you get older.

FEGLI can be cancelled at any time. Please don’t cancel FEGLI before you have another insurance policy in place, though!

FEGLI can be obtained or increased at any time. However, if it’s not during an enrollment period(which is extremely rare), it is subject to underwriting rules, meaning a physical, etc.

FEGLI can be carried into retirement, but rates and coverage may change depending on your election of coverage. All premiums during your working years are paid each pay period. In retirement, you can only pay premiums monthly. Most private insurance companies will quote premiums monthly or annually. So when comparing plans, make sure you are comparing apples to apples, i.e., monthly premiums to monthly premiums. Don’t make the mistake of comparing pay period premiums to monthly premiums.

So why is all this important? I mean, really, what’s the point? Well in these days of increased talk of reducing our retirement benefits, it is more important than ever to make the smartest financial decisions possible regarding those benefits. To be able to save $20,000 or more over two decades means more money for TSP contributions, 529 savings, paying off student loans or credit card debt, or simply letting compound returns work harder for you in your brokerage account.

Thank you so much for reading all this. I never take it for granted for a second how valuable your time is. I sincerely hope it helped you become a better informed federal employee. Feel free to contact me regarding any of this and feel free to check out some of the links below, which provided most of this information.

RESOURCES

SF-2817 Life Insurance Election. For changing FEGLI Insurance.

SF-2818 Continuation of Life Insurance Coverage. For electing life insurance in retirement.

SF-2823 Designation of Beneficiary. For designating/updating a beneficiary.

This is meant to be informative. It is not financial advice. I am simply trying to show you how much FEGLI costs. What you do with that information is up to you, your financial planner, your spouse, and your life insurance agent. Determining how much life insurance you need, and what type, is best discussed with a financial planner and/or insurance agent, as there are many factors that come into play. There are a dizzying array of life insurance products; I’m not endorsing any particular product or company. In the end, FEGLI may be best for your financial situation, but please consult a professional.