We need to tackle the big scary monster that lurks in every retirement conversation: long-term care costs.

You’ve probably heard the frightening statistics. “The average cost of a nursing home varies significantly by location, but recent data from 2024 shows a national median cost of around $116,800 per year for a private room and $104,000 for a semi-private room.”

These astronomical figures make you want to stuff every penny under your mattress “just in case.” People love to use the cost of long-term care as the ultimate conversation stopper when discussing retirement spending, as if mentioning it automatically proves retirement is an impossibility.

But here’s what you need to do: take a deep breath and look at the actual numbers. Not the scary headlines, but the real data about what happens to real people.

The Numbers That Matter

Let’s start with a simple question: How many Americans over 65 are actually in long-term care facilities right now?

According to the CDC, there are currently 1.3 million people living in nursing homes across the United States (Table 4 in link). Now, here’s the surprising part: 17% of those residents are actually under 65. That means we have just over 1 million Americans over 65 in nursing homes.

To put this in perspective, there are over 61 million Americans over 65 today. So we’re talking about 2% of seniors currently in nursing homes. .

Add in assisted living facilities, which house about another 1 million residents, and we get to roughly 2.5 million people in institutional care. That brings us to about 4% of the over-65 population. The financial industry would have you believe this number is closer to 40%.

The Home Care Confusion

Now, this is where things get deliberately misleading in the fear-mongering department. You’ll often hear that over 10 million people over the age of 65 receive in-home health care as well as how expensive it is.

But hold on. Of those 10 million people, how many are actually writing checks for professional in-home care services? This detail is conveniently overlooked.

Many people receiving “in-home care” are being helped by spouses, adult children, or other family members. Others might need only minimal professional services. The vast majority aren’t paying anything close to those headline-grabbing numbers that are used to scare people.

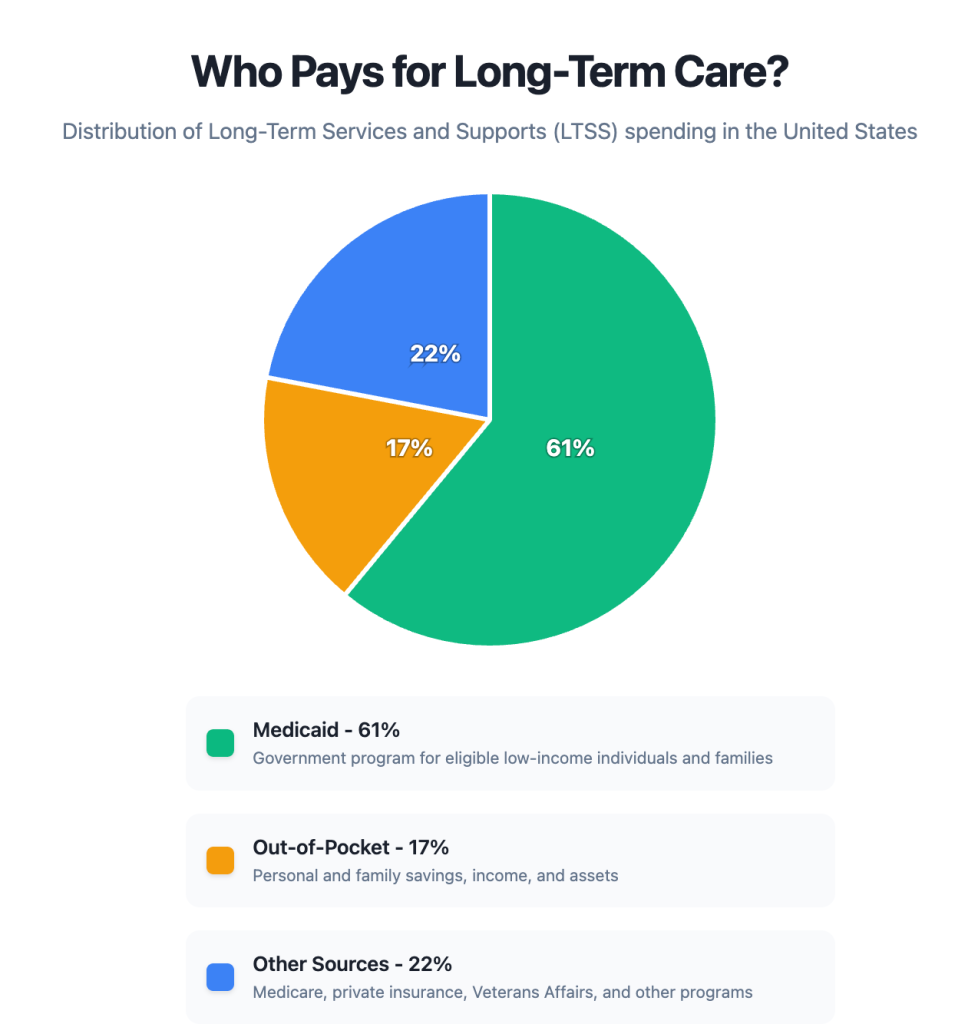

Who Really Pays?

Even among those who spend considerable money on health services, most aren’t shouldering the full financial burden themselves.

The majority of long-term care expenses are covered by insurance programs—primarily Medicaid and Medicare, along with private insurance. Out-of-pocket spending, while significant for those who pay it, represents a smaller slice of the total long-term care spending pie.

The Time Factor

Even if you do end up needing facility-based care, you probably won’t be there as long as you fear.

A study by the National Institutes of Health found that among people who died in long-term care facilities, the average stay was 13.7 months. But that number is skewed by a small group of people who stayed much longer. The median stay—which better represents the typical experience—was just 5 months.

More telling: 65% of people who entered facilities stayed less than one year, and 53% died within six months of admission:

“(of the people who died while in a facility) the mean length of stay among decedents was 13.7 months; however, this was explained by a relatively small number of subjects with long lengths of stay. The median length of stay was only 5 months (IQR 1-20). The majority of residents had short lengths of stay, 65% percent of decedents had lengths of stay of less than one year, and over 53% died within 6 months of admission.”

Putting It in Perspective

Let’s step back and see the full picture:

- Only 4% of seniors are currently in institutional long-term care

- Maybe 10-15% of seniors pay significant amounts for any type of long-term care

- Most long-term care costs are covered by insurance programs, not personal savings

- When facility care is needed, it’s typically for less than a year

This doesn’t mean long-term care costs don’t matter or that you shouldn’t plan for them. It means they shouldn’t dominate your entire retirement financial strategy or prevent you from enjoying the money you’ve worked hard to save.

The Bottom Line

We have a tendency to plan for the worst-case scenario as if it’s the most likely scenario. But the math tells a different story. The overwhelming majority of retirees will never face catastrophic long-term care expenses.

Yes, you should have a plan for long-term care—whether that’s insurance, setting aside some funds, or understanding your family’s health history. But you shouldn’t let the tail wag the dog. Don’t let a small probability of high costs prevent you from making smart decisions about the money you’re far more likely to actually spend.