My man Todd sent me the latest update from Vanguard for their “Preliminary estimated year-end distributions”. There were some big surprises I must say.

What we see is a number of funds distributing well over 5% of their Net Asset Value (NAV). To put this simply, let’s say a fund/ETF has a share price today of $100 and it expects to distribute $7.50 in realized capital gains. That means its distribution is 7.50% of NAV.

Quiz time: Your fund has a price of $83 and it’s about to distribute $10.20 in capital gains. What is its distribution as a percentage of its NAV? Answer is at the bottom of this post.

Generally speaking, when we have a significant market crunch you’d expect to see fewer funds with large capital gain distributions due to the fact that prices of their holdings have dropped significantly. Just look at Facebook for Heaven’s sake. It’s down, what 70% or something, year to date. Crazy.

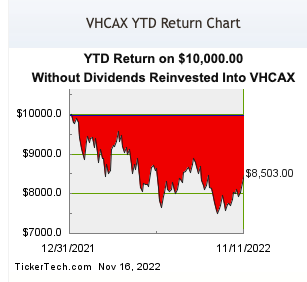

Yet let’s take a deep dive and look at the Vanguard Capital Opportunity Fund. It’s down 15% year-to-date.

Even with that decline in price it’s still going to distribute $12.30 a share on 12/20. As of today, with a share price of $165.95 that means the distribution is equal to 7.41% of the fund. That’s a huge Capital Gain for those unprepared. What if you held this in a brokerage account and you are getting Obamacare subsidies? This distribution could cost you big time!

Yet many investors may be unaware of such distributions because the market is down this year. “Who could possibly have capital gains this year when we are/were in a bear market?” Funds that have been buying, and holding, for years, that’s who!

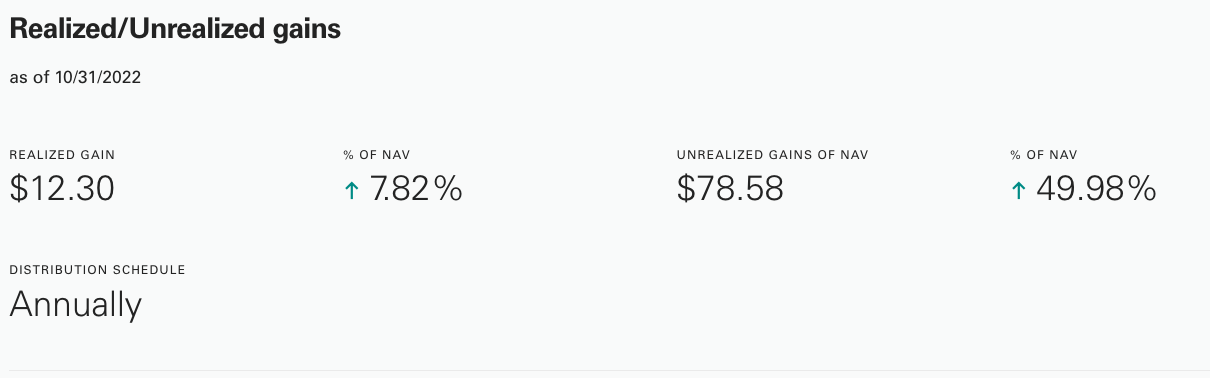

Look at the above. That’s the VHCAX unrealized gains that have been accumulated in the fund over the years. 50% of the portfolio’s value is due to accumulated gains that have yet to be paid out and thus yet to be taxed.

Go back to my blog post from the other day “Markets Are Down! You sure about that?”

Seeing the unrealized gains in the Vanguard Capital Opportunity fund just confirms my point. You aren’t down if you’ve been in the market for at least 2 years. The taxes you’re going to pay is just more proof. You don’t pay taxes if you have no gains. It’s literally that simple.

I invite you to look through the linked Vanguard piece to see what your Vanguard funds will pay out. Notice even Good, Ole Wellesley Fund will pay out over 4% of its NAV in capital gains. Wellington will pay out nearly 6%.

*** Remember capital gain distributions are NOT dividends or interest from bonds. Those are other sources of income, aka taxes, from your holdings***

The problem, of course, is for investors who are seeing negative values in their portfolio and then get hit with a tax bill. They’ll scream bloody murder “how can I pay tax when I lost money!” I’ve seen this in my own career many, many times.

I’ll never forget a lady who came into my office here in Alpharetta, GA back when I was working for USAA. She dumped her American Century mutual fund statements on my desk and said “how can this happen? I’m down 20% this year yet this statement says I’m going to have to pay $6,000 (or whatever it was) in capital gain taxes!” Initially it seemed she was angry at USAA even though we had nothing to do with it.

But we got to talking and I showed her what was going on. She had purchased an American Century fund for we’ll just say $10. Fast forward in time and it went to $50. But the next year it fell to $40. Thus she was still up $30 a share but in her mind she was down $10. So she was shocked to get a tax bill when she was down $10. Again, this was the way she was seeing it and wrong as she was, it still ticked her off because she “didn’t know how it worked when (she) was sold the funds.”

Mind you, she never griped when the funds were up. Similar to when people gripe about the “volatility” of the stock market. Volatility is a two-way street of course. No one is upset when it’s volatile as long as the markets are up, only when it’s down. Weird. 🙂

Anyway, I also had to point out that the $6,000 in capital gains wasn’t the actual tax she’d have to pay. It was just the total gain she had and she’d only pay a percentage, if anything, of that. Turns out she was still in the 12% bracket so she wasn’t going to have to pay any capital gain tax anyhow.

So she left my office feeling much better. But how many people are just like her, maybe even you, who don’t know how your investments are actually taxed? Even worse though is for people who buy a fund, say in 2022, watch it drop and still get hit with the capital gain distribution! That happens all the time. They weren’t even in the fund for the run up, from say $10 to $50. They just were in it for the drop from $50 to $40 and still have to pay the tax man.

Them’s the rules, folks. As they say, ignorance of the tax code is no excuse. You own the investment, you pay the tax. But be merry. To reiterate the reason you pay tax is because your fund made money. Most likely YOU made money too. If you are paying tax for money your fund made but you didn’t, well, I simply ask “where have you been these past 12 years?” The money was there for the making. All you had to do was BE IN THE GAME. Let that be the lesson.

*** Answer to the quiz – 12.28% ***