Check this Out:

(We’ll be talking about this chart and many other things Social Security related on the live stream today at noon eastern. Here’s the link for the “Big” channel if you will. And here’s the link for the back up channel. I encourage you to subscribe to both.)

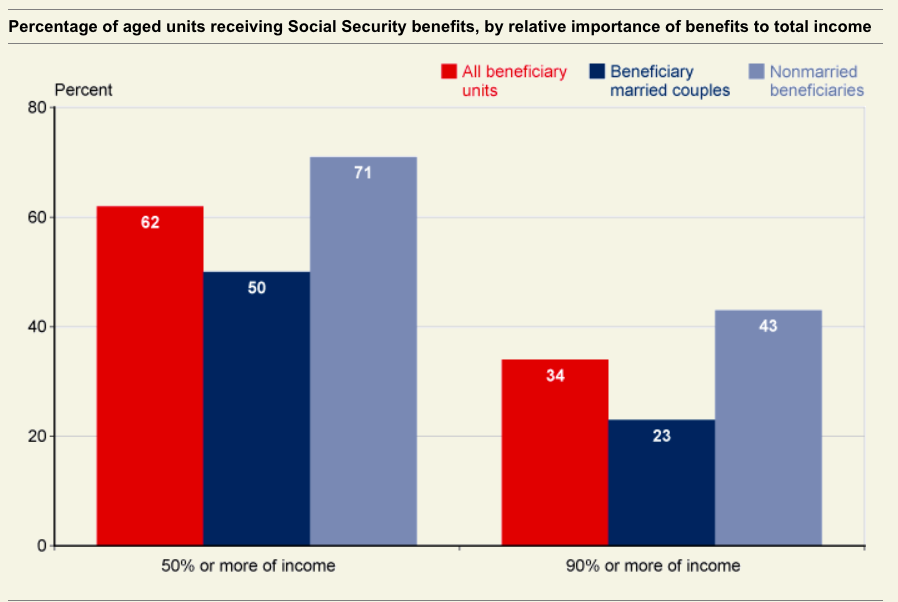

That chart from the Social Security Administration shows that in 2015 62% of the aged population relied on Social Security for over HALF their income. 34% of the aged relied on Social Security for over 90% of their income.

Wow. That’s a lot of people who have no income other than Social Security, proving that people just aren’t saving enough and retirement is a pipe dream for most of us. After all, everyone knows you can’t retire only on Social Security! (Shameless plug, obviously they haven’t read my book You Can RETIRE on Social Security which you can get here.)

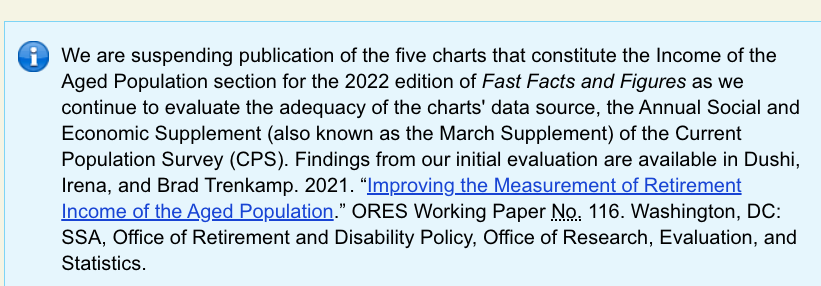

But going back to that chart, it’s from 2015 so hopefully things have changed since then right? Well let’s see. So I click on the link for the 2022 version and this is what I get:

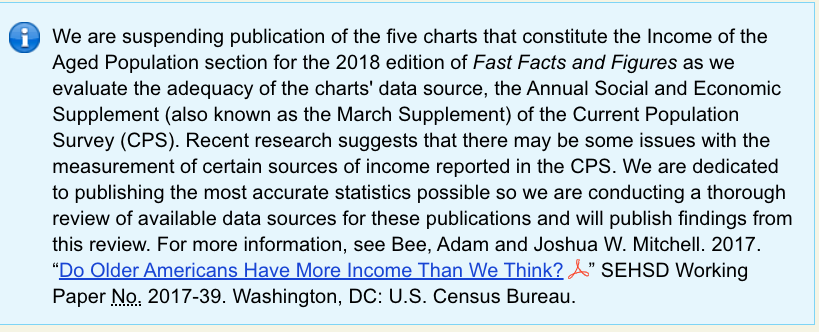

Wait, what??? How long has this been going on? So, I all the way back to the 2018 version and I get this:

Same message, just a reference to a different paper to make the point: The Census Bureau, which Social Security has used in calculating its data sets has under-reported actual income from retirees for years.

Did you know that: “For years, there has been an ongoing discussion about the underreporting of retirement income in the CPS, with a wide acknowledgement that although underreporting exists…” I bet you didn’t.

Did you know that: “among all households headed by an individual aged 65 or older in 2012, median household income was 30 percent higher in the administrative records than in the CPS ($44,400 versus $33,800.” That’s a 33% INCREASE in retirees income that was just overlooked. Weird, huh?

Even weirder are the crickets among financial professionals when it comes to this stuff. It’s not like this is new info after all. I’ve done videos on this exact topic going back to 2018. Yet, anyone else? Nope, crickets.

And, for me, as a “pro” financial planner since 1998 this complete ignorance of this topic by my peers really ticks me off. If this was 2018 or 2019 and no one was talking about it, I could understand. It was a relatively new concept uncovered by Census Bureau economists which ultimately made its way to the Social Security Administration. But this is the 4th quarter of 2022 for Heaven’s sake! And for the financial planning industry to continue to either ignore or be ignorant of one of the most positive pieces of news in retirement planning history just proves, once again, the lack of seriousness in our industry.

We are an industry composed of investment managers, not much else, I am afraid to say. Even after all these years of promoting the CFP, “holistic” financial planning, etc., when the rubber hits the road it’s investing that drives everything.

And as such, until the financial industry stops charging fees for assets it will never be a real industry the way we want it to be. When investments pay your bills what do you think you’re going to focus on? Investments of course.

Social Security doesn’t pay the bills so Social Security is an afterthought to the industry. Yet while we now know Social Security doesn’t account for over 50% of the income for 62% of retirees as the first chart shows it still is the second largest source of income for the average retiree.

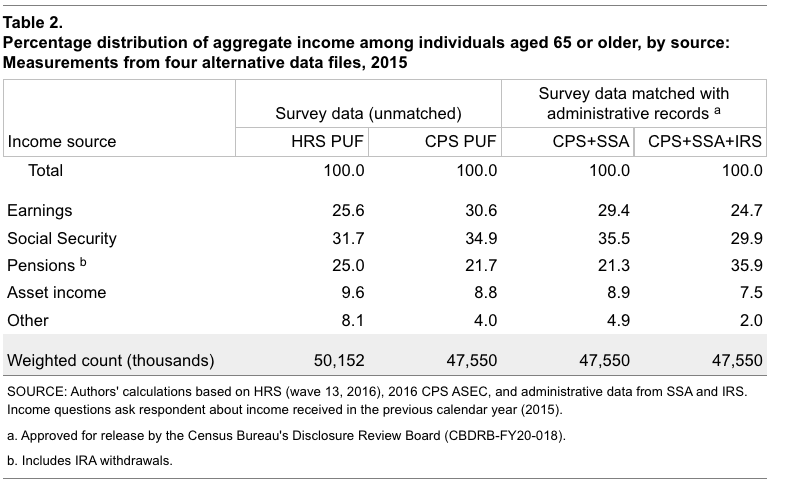

See the chart below and look to the far right column, where it says CPS-SSA-IRS. That’s the most thorough represenation of where retirees get their money.

Now, notice in the first column the word “Pensions” and you’ll see the small letter b.

Go to the bottom of the page and you’ll see that b says “includes IRA withdrawals”.

And that’s the crux of the matter. The CPS, Current Population Survey from the Census Bureau, greatly underreported IRA withdrawals. If you actually read the questionnaire given to respondents you could see why people were confused about their income sources.

So, when the researchers noticed the discrepancy between tax data and the CPS they realized the problem and have looked to other data sets to adjust. Hopefully the CPS will adjust its questionnaire too but given it’s been over five years I wouldn’t hold one’s breath.

Either way, the point is that retirees have a boatload more income than is previously reported. Is it any wonder that 80% of retirees are satisfied in retirement? You’d think there would be a bunch of retirees down at the soup kitchen given all the negativity we’ve been told about people’s inability to afford retirement. There’s not though. Weird, huh?

But, again, my issue is with the Retirement Planning industry. They(we) should be on the forefront of this! This is our flippin’ job after all to prepare people for retirement. But nope, we’re too busy looking up the latest and greatest in investment “research” as if that’s going to do anything for anyone. We’re still busy harping on the 4% “rule” because it’s easy and everyone uses it. It’s industry standard after all.

We’re too busy talking about modern portfolio theory, efficient market hypothesis, Markowitz, French/Fama, Shiller etc. as if any of that matters when it comes to an actual real person’s ability to retire.

So doggone frustrating And sadly it will always be like this until we separate fees from investments. It’s just that simple. Yes there are some deep thinkers in the business. A few. Way too few though and given the amount of ink that is spilled you’d think there’d be more actual students of the business. But there are not. There’s tons of students of the business of investing, don’t get me wrong. But that’s basically worthless, as Malkiel showed way back and John Bogle too, of course.

I’ll just keep doing my little thing on Youtube, until they ban me, talking about the IMPORTANT stuff. Wake me when the rest of my industry decides to join me, please.

See you at noon!

Blessings,

Josh