“My wife is so stressed at her job but she can’t quit because of health insurance.”

Oh man, if I had a nickel every time I was told something like this, I’d have a million nickels! 🙂

Look, as much as I didn’t like Obama as President, and certainly don’t like Nancy Pelosi as Speaker of the House, then(2006-2010) or now, the fact is that Obamacare is the law of the land. Obamacare was actually PASSED by both houses of Congress and signed into law by the President. (This is the way politics is supposed to work in America by the way. Not a dictate by some unelected and unaccountable Public Health official, if you know what I mean.)

Obamacare is the landscape we’re operating under. Yell at the clouds if you must but let’s deal in reality shall we?

So, let me paint a picture of a couple I was working with the other day. They want to move back to their native state, we’ll say Montana, just because it’s rural. They are not even 60 years old yet so they know they’re going to have to go on the Exchange for health insurance. Yes, they could go the Medishare route but with pre-existing conditions that might not be the best option.

They had budgeted $24,000 a year for health costs until Medicare kicks in. They had also budgeted $6k a month in discretionary expenses AND another $2k a month for their mortgage. Essentially they assumed they’d spend $10k a month until Medicare.

***SIDE BAR***

When I initially ran their numbers they were only at a 7% probability of not running out of investable assets before they died. I was a bit nervous because their move was ALREADY in place as they had both already quit their jobs. YIKES! It’s never fun for a financial planner to tell folks who have over $1million in liquid assets that they’re going to need to tighten up.

Thankfully, that $6k a month in expense actually INCLUDED health care costs and their mortgage. They were double-billing themselves on expenses! No wonder their probability of success was so low. When we undid the double billing they are looking just fine even with $24k of annual health costs. But see below for how even those health costs were WAY over estimated.

***END OF SIDE BAR***

Let’s just assume these folks will move to Billings, Montana. A smallish city of only 100k or so. But it is the largest in the state of Montana. Take note that there is no major university in Billings. Yes, satellite campuses but that’s it.

So, we have a small town, in a very rural state with no major universities. Hope you see where I’m going here. Not the best environment for insurance companies to want to do business and really not a great environment for PROVIDERS to set up shop either.

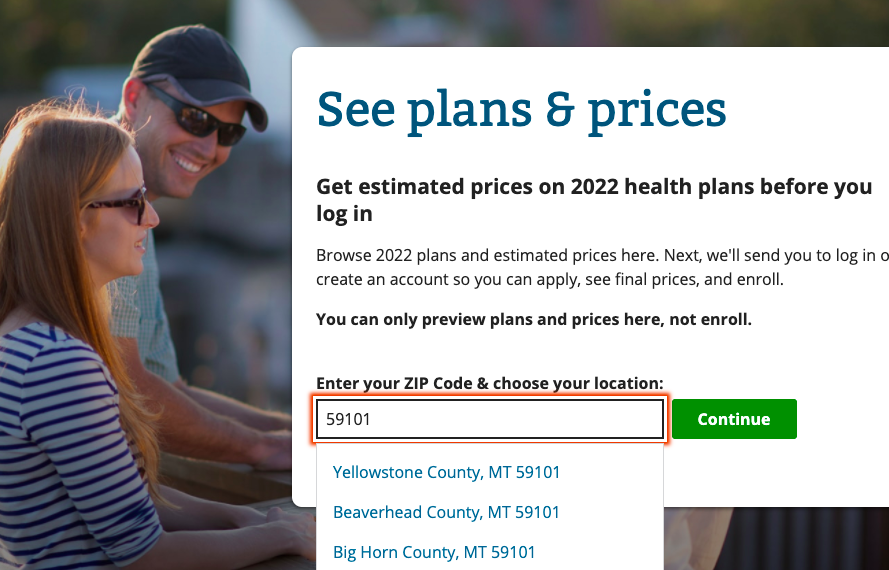

Yet, and here’s where it gets real interesting, we go to HealthCare.gov and search plans available by zip code. For Billings we’ll use 59101 and click Yellowstone County.

Now, we’re going to tell the system about ourselves. Click the green START button. Assume you’re NOT enrolled in a current Obamacare plan and hit SKIP.

Next you’ll enter your data. If you’re married click the radio button that says “YOU AND OTHER PEOPLE” if you’re single just click “YOU”. Hit continue.

In this case, I’m entering the age of 58 for the hub and again for the wife and click the button that says “NONE OF THE ABOVE”.

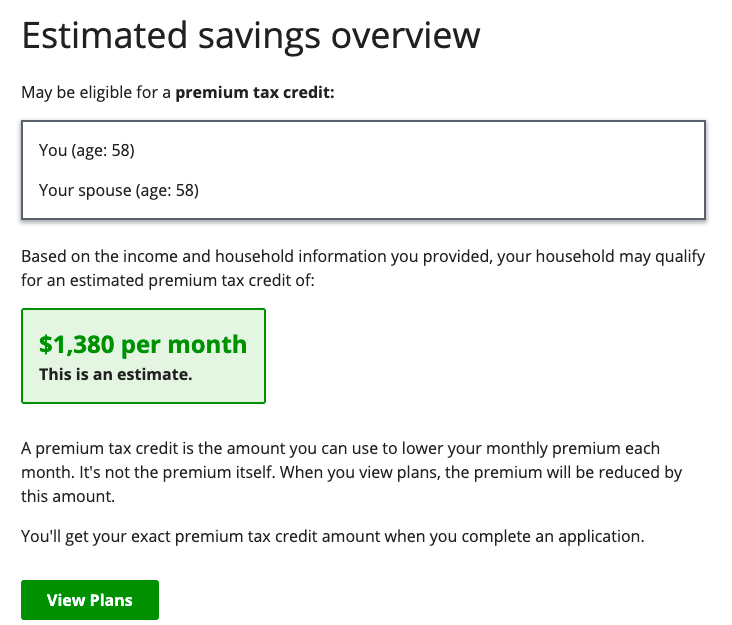

Next you’ll come to the place to enter your estimated 2022 income. In this example I’m putting $60,000(more on that in a different blog post).

And this is what we get:

Click View Plans – NEXT – SEE ALL PLANS and you’ll get a list of 27 plans to choose from, 24 are PPOs.

The premiums range from $0 a month to over $800 when factoring the premium credits. What’s the difference between these? I have no idea. But this would be something you’d want to investigate, no?

I am literally looking at 24 plans, all PPO’s available to these folks at costs SIGNIFICANTLY less than what they were anticipating.

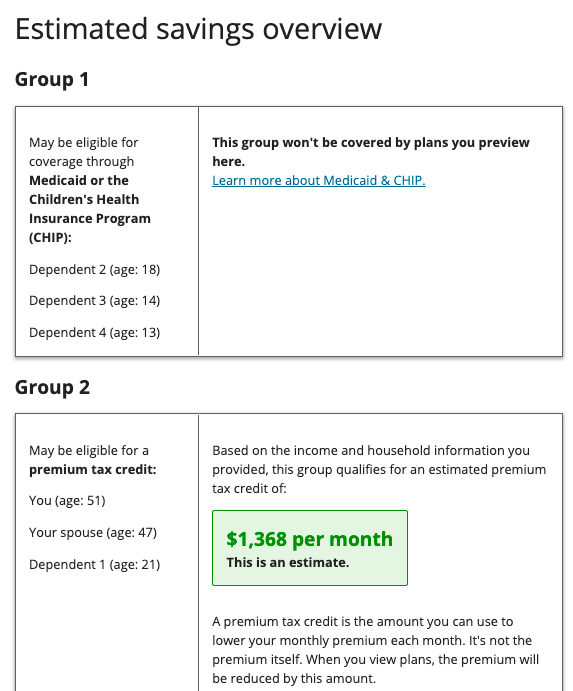

Do you think only people in Billings, Montana have these options? I highly doubt it. Let’s say you live in the Atlanta, GA suburbs as I do. And let’s say you have 4 kids, as I do.

What do you get then?

Here you’ll notice my 3 youngest kids don’t qualify for Obamacare but they do Medicaid. Why? Because I stated my income was $60,000. $60,000 with a family of 6 puts me in low income status, too low for half my family to qualify for Obamacare. I don’t want that. So, I need to increase my income.

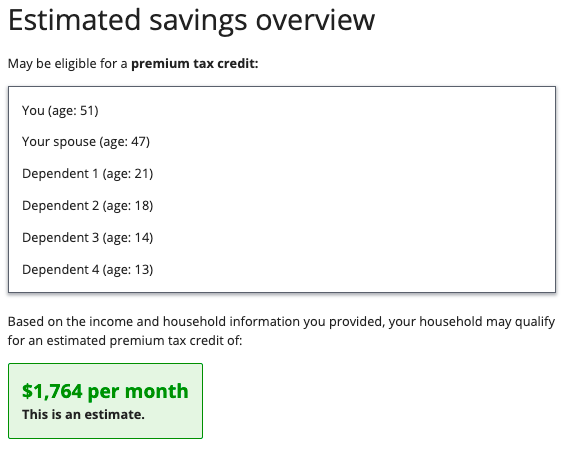

Now at $100k, I get full Obamacare coverage for my entire family AND premium credits of over $1,700 a month.

There are 142 plans available! Unfortunately, they are all HMOs. Now, is that the end of conversation? OF COURSE NOT! Maybe an idea is to get on the HMO for catastrophic coverage but align yourself with a concierge Primary Care Doctor with all the money you save because of premium credits.

I just signed up with a concierge doc through PartnerMD. My first meeting will be on Thursday. I’m looking forward to it.

The concierge doctor for just me costs about $2,000 a year. I imagine there will be discounts when my whole family is added. But we’ll see.

The point is that there are SO many opportunities now for health coverage without solely relying on your employer. Why are you not at least looking at this? Especially, if your work is literally KILLING YOU!?!?!

And we haven’t even talked about Medishare or the other faith-based co-insurance plans that are out there.

Finally, let me just tell you how many people actually get physically WELL once they quit their crappy, old jobs. They lose weight. Their blood pressure drops. They sleep better. They eat better.

It’s almost like work is making you sick and that’s why you stay at work because work provides you the insurance to deal with the sickness that work is causing. It’s crazy. Kind of like Big Pharma, you need pills to deal with pills they’ve given you before to deal with issues that are related to your work.

You really need to find the SOURCE of your discontent. Once you the target has been isolated, see how you can eliminate it from your life. But for Heaven’s sake, stop being a pawn and just taking the path of least resistance. Yes, this will require some effort on your part. Getting up every day to go to a job you hate isn’t effort?

To quote our esteemed Prez “Come on, man!”

Blessings,

Josh